Introduction

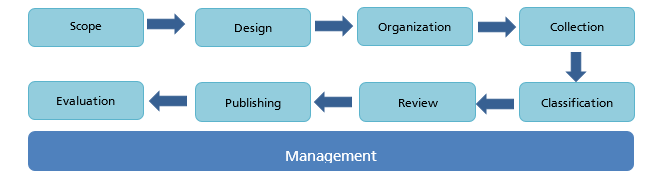

First: Scope

Second: Design

Third: Organization

Fourth: Data collection

Fifth: Data disaggrregation

Sixsth: Revision

Seventh: Publication

Eighth: Evaluation

Ninth: Management

Introduction:

In all its statistical work, GASTAT applies a unified methodology suitable for the nature of each statistical product using the Statistical Procedures Guide approved by international organizations. Statistical products undergo 8 main phases, in addition to a ninth comprehensive phase, “Management”, as shown in the following diagram and explanation underneath:

The first 3 stages (Scope, Design and Organization) are a cooperative process between GASTAT and its clients, represented by developmental entities data users, while Phase 4 (Data Collection) is done through GASTAT’s cooperation with the statistical population, whether families, businesses or holdings, in order to complete data and information. The remaining phases are statistical stages in which data is classified, reviewed and published. Then, Phase 8 (Evaluation) is carried out with clients. The Management Phase it is an administrative and organizational procedure applied across all phases. These phases have been applied to national account indicators as follows:

First stage: Scope:

The starting point of the preparation of the (Industrial Activity Survey) and the first shared phase between GASTAT and other stakeholders from relevant entities, represented in (Ministry of Energy, Industry, and Mineral Resource, Economic Cities Authority, Industrial Development Fund, Ministry of Commerce and Investment, and Royal Commission for Jubail and Yanbu). At this stage, a number of meetings and workshops were held between GASTAT and those entities to understand their needs and requirments. Their feedback were also considered to ensure the realization of all the objectives of the survey, which are:

- Measuring the relative contribution of the industry activity to GDP.

- Providing detailed data on the industry sector.

- Showing the changes in production overtime.

- Provide data on workers in industrial activity by gender and nationality.

- Provide data on the amount of compensation paid to employees.

- Provide data on expenditure and operating income of industrial activity.

- Identify the energy use of electricity, water and fuel.

- To know the extent to which the industrial sector contributes to research and development spending.

- Identify the challenges faced by enterprises operating in the industry.

- Identify the types of investment plans for the facility.

- Knowledge of the incentives and financing obtained by industrial establishments.

- Meeting the needs of government agencies, the private sector and researchers for data and statistical information.

- Conducting regional and international comparisons in order to know the kingdom's ranking in manufacturing.

moreover, the statistics of this survey will contribute to Saudi 2030 Vision, it will also cover international and regional requirements represented in the Sustainable Development Goals (SDG).

Second stage: Design:

During this stage, a complete design for the statistical product in addition to the tools and methods of data collection, statistical community , survey form, sampling units are all set forth. Beneficiaries are engaged in all these processes to take their feedback into account, so that the product would live up to their expectations.

The most important outcomes of this stage are

1. Satatistical population:

The target statistical population within the survey is composed of all economic establishments included in the International Standard Industrial Classification of All Economic Activities (ISIC-4) in the Kingdom.

2. Sataistical sources:

Data of the survey is based on the field survey conducted by GASTAT on a yearly basis and are listed under the classification of (economic statistics). Data is collected in the survey through visiting a sample of establishments that represent all administrative regions of the Kingdom of Saudi Arabia, as well as completing an electronic questionnaire that includes a number of questions. Estimations and indicators are provided within the survey in relation to Industrial Activity Survey.

3. Concepts and terms related to Industrial Activities Survey:

3.1. Industrial activity:

It is all that is practiced or offered by the economic establishment under mining, quarrying, manufacturing, electricity, gas, steam, air conditioning, water supply, sanitation, waste management and remediation in all regions of Saudi Arabia. The classification of the establishments’ economic activity is based on ISIC REV.4 with limited modifications to suit the institutions operating in Saudi Arabia.

3.2. Workers:

All individuals (Saudis and foreigners) who already work for the establishment with or without pay, as well as the owners, their affiliates and users, whether they are full-timers or part-timers, permanently or temporarily employed, males or females, whether they are paid on a daily, weekly or monthly basis. Workers also include partners and members of joint-stock companies, board chairmen and members, as well as workers on paid vacations.

3.3. Raw materials:

They refer to production inputs or crude materials used to manufacture products. Such unprocessed materials may be renewable or unrenewable.

3.4. Production:

A general term for all activities involved in providing commodities and services by way of converting inputs into outputs..

It is defined as the process of manufacturing raw materials to be consumables, such as commodities and services, in order for the establishment to make profit.

The production process is also defined as the movement of production elements movement through which the community needs are met. Actually, such operation has many phases starting from manufacturing of raw materials, through to the exchange, ending up with the consumption process.

3.5. Commodities:

They cover tangible merchandise of final consumption purchased by the consumer. They could be divided into durable and non-durable commodities. Commodities could alternatively be defined as: "a set of benefits obtained by consumers to meet their needs”.

3.6. Establishment characterstics:

- Single: It means that the establishment has no branches.

- Head Office: It means that the establishment has at least one branch.

- A branch with independent accounts: It means that the establishment has accounts separate from the head office.

- A branch with no independent accounts: It means that the establishment does not have accounts separate from the head office.

3.7. Employees‘ payable remunerations :

The due regular amounts paid by the establishment to its workers throughout the year, such as wages and salaries payable in consideration of the normal working hours, fixed bonuses together with all benefits and allowances such as accommodation, social insurance or transport allowances.... etc., including:

Commodity requirments:

The values of all local and imported goods supplies used by the establishment either in productive goods installation (such as electricity, water and raw materials consumption), or the goods required for their production. It also includes the values of stationery, spare parts, fuel, oils, electricity and water consumption costs ... etc., or any other goods supplies with mentioning the types of such goods for necessity.

Services requirements (industrial and non-industrial operating expenses):

The values of all service requirements that the establishment uses including maintenance and repair costs, contract work, post office and telephone costs, training and secondment costs, travel costs, machines and equipment rent costs, premises and non-agricultural lands rent costs, and what the establishment pay for legal consultations or for services provided by others ... etc., or any other service requirements with mentioning the types of such services for necessity.

3.8. Transformational expense:

refer to all paid or payable amounts by the establishment during the year in connection with the establishment current activity and not related to the goods and services requirements such as compensations, fines, dividends, insurance premium, Zakat, donations, customs duties ... etc., or any other transformational expenditures with mentioning the types of such expenditures for necessity.

3.9. Operating revenues (industrial and non-industrial):

All cash revenues earned by establishment as a result of providing services for consumers, including, revenues from contract and commission work, maintenance, repair and installation work. The operating revenues also include the revenues from secondary activities and the sales of goods purchased for the purpose of reselling them in in the same condition. This also includes revenues of selling manufacturing wastes and renting buildings, non-agricultural plots and machinery etc., and any other services provided to others.

3.10. Transformational revenues:

It is all collected or due revenues of investments returns or projects profits, such as shares and participations profits, collected interests, capital assets sale profits ... etc., and which is not the output of the practice of the main economic activity or other secondary activities. It also includes governmental subsidies and donations offered by others, in addition to compensations collected from insurance ... etc., or any other transformational revenues with mentioning the types of such revenues for necessity.

3.11. Alteration in assets and liabilities:

Measuring the assets book value and the changes that may occur to the assets in the form of purchased additions, or from the own-production after deducting the sales, or the excluded assets and the annual depreciation value. The book value shall be registered at the begging and at the end of the year.

First: non-financial assets:

Non-financial assets are divided into main and sub categories:

Fixed (productive) assets:

Refer to the assets owned by the establishment for conducting production operations, accomplishing its services, or for facilitating its business operations (and not for re-selling them), as the assets are kept as long as they are productive, such as properties and machines. These assets have some advantages: They are not usually used up in a sole one year. Additionally, they have the same way of evaluation and the same purpose. They are also funded similarly as they are usually funded by project owners, or by partially long term loans. The fixed assets are::

- Residential buildings

- Non-residential buildings

- Means of Transportation

- Equipment and machinery

Fixed (non-productive) assets:

They are the assets that cannot be reproduced, and they include the following :

- Land

- Researches and studies

- Rent and licensing contracts

- Brand name

Inventory

The stock consists of the products sold by the establishment as a commercial activity, or the raw materials the establishment utilizes in production process. This stock is one of the biggest assets in commercial and industrial establishments. The commercial goods of the establishments are often ready and do not need much work and service to be ready for sale. As for the industrial companies the case is different as these companies have different types of goods according to the stage goods go through till they reach the ultimate form as a good ready to be sold. There are the raw materials, the to-be-manufactured stock, and the finished products stock. These three items are demonstrated in detail in the budget, or as a group under the stock section. The stock is evaluated by cost or net market value. The stock section does not include goods deposited at the establishment for sale, and it is divided as follows:

- Goods purchased for re-sale in the same condition.

- Raw materials, spare parts and packaging materials

- Finished products

- Non-finished products

Second (financial assets) including the followings:

- Deposits and cash balances in banks and the fund

- Securities

- Loans (include debtors)

- Stocks and shares

- Other account receivables

Third: financial commitment:

They refer to the establishment financial commitments to others such as vendors, lenders, and owners. They include due commitments (payable notes, creditors, commercial vendors, and accrued expenditures). These deductions have a shared characteristic as they are usually used to fund current assets. As financial assets, financial commitments are likewise divided into main groups, and secondary groups, such as:

- Securities

- Loans (include creditors)

- Stocks and shares (Shareholders' equity)

3.12. Legal entity:

The company established in Saudi Arabia shall take one of the following form :

- Joint Venture Company

- Joint liability company

- Limited partnership LP

- Partnership limited by shares: it consists of two teams of partners

- Joint-stock company JSC

- Limited liability company LLC

- Other: any legal form that the company may take other than the above

3.13. Share of ownership of capital:

Identify the shares of the participated sectors by nationality for the capital

3.14. Financial assets and liabilities by regulatory sector:

- Non-financial projects: all the projects operating in all economic activities except for money and insurance

- Financial projects: are the operating units in the financial intermediary services and other related services which include (banks, insurance, brokerage services, money exchange and other financial services)

4. Used statistical classification:

Classification is defined as being an arranged set of related categories used for data collection according to similarity. It is the basis for collecting and publishing data in all statistical fields, such as economic activity, products, expenditures, jobs or health, etc. It allows for classifying data and information through putting them into meaningful categories to produce useful statistics, considering that data collection requires precise and methodological arrangement in accordance with their common features so that the statistics can be reliable and comparable. The finance and insurance survey is subject to international standards in terms of collecting and classifying its data as it uses the following classification:

First: The International Standard Industrial Classification Guide for Economic Activities Coding (ISIC, Rev.4):

The updated economic activities guide is divided into (17) sections, each section is consists of (60) divisions, and each division is divided into (154) category. The new division of this guide facilitates any future updates in the guide, as well as the creation of new codes for the branches of activities at the level of more than five sections in accordance with future requirements.

Second: Central Product Classification (CPC2):

CPC forms a complete classification for products including goods and services. Purpose of this classification is to create an international standard for collecting and categorizing all types of data that require some details of the product, including the industrial production, national accounts, services industries, internal and external trade of major goods, international trade in services, payments balance, consumption, prices statistics. In addition to other main purposes such as: provide an international comparable framework, activate the coordination between various types of statistics related to goods and services.

Third: International Standard Classification of Occupations:

Persons are categorized according to their actual and potential relationship with jobs. Jobs are categorized according to the work performed or to be accomplished. The primary criterion for classifying the system into major and sub-groups is the level of skills and specialization required to carry out work and tasks related to the profession, with separate main groups for senior officials, managers and the armed forces.

5. Design of survey questionnaire:

The survey questionnaire was drafted and designed by industrial statistics experts at GASTAT. International recommendations, standards, and definitions were taken into consideration during the design of the questionnaire, which was presented to experts and specialists, as well as to relevant entities to obtain their insights and comments. Questions were redrafted based on a specific scientific approach aimed at unifying question formats used by researchers.

|

The questionnaire was divided into 14 sections by topic to improve the efficiency of complying with technical standards during the fieldwork stage. |

||

|

Data on the establishment |

Economic activity |

Number of workers during the year |

|

Operating expenses (used goods and services during the year) |

||

|

Production by type of goods |

Operating revenues |

Change in assets and liabilities (in thousand riyals) |

|

Quality managment |

Holding type |

Total occupied area |

|

Production capacity used |

Does the establishment have any investment plans |

Does the establishment work in research and development |

|

What are the main problems facing the establishment right now (list three main problems) |

||

|

A full copy of the questionnaire can be viewed and downloaded via: |

||

After being approved, the survey questionnaire will be transformed into an electronic questionnaire that can be handled through the advanced data collection system using tablet devices. The system has the following features:

- Reviewing the work zone of the field researcher (survey sample).

- Reaching the sample (establishment) using the map on the tablet device.

- Completing data of highquality using data check rules and navigation (to automatically detect input errors and illogical inputs while the completion of the data is underway).

- Establishing communication between supervising entities by exchanging comments with field researchers

6. Coverage:

6.1. Spatial coverage:

The finance and insurance survey covers data related to finance and insurance activity in all 13 administrative regions of the Kingdom of Saudi Arabia, which are: Riyadh, Makkah, Madinah, Qassim, Eastern Region, Asir, Tabuk, Hail, Northern Borders, Jazan, Najran, Al-Baha, and Al-Jouf. The focus was on cities since they include around 84% of establishments in Saudi Arabia and around 91% workers as well. A scientifically selected sample is visited in each region representing the region’s establishments that practice financial and insurance activities.

6.2. Temporal coverage:

It is carried out during the period set for visiting the targeted establishments of the survey sample and completing the survey questionnaire data. The survey data are usually associated with the year that precedes the period of conducting it.

7. Statistical framework:

Designing the statistical frameworks ‘plan:

- The updated 2015 census of the 2010 Establishment Census was used as a list containing all population items

- The lists, maps and analytical standards of the units were set to choose data providers (establishments).

- The required descriptive data were identified in order to create the statistical framework, create the test framework, verify them, and use them for the current survey round.

8. Sample design:

8.1. A perfect plan is designed and documented to choose the sample units from which data will be collected with providing guarantee for obtaining efficient and highly effective estimations. Therefore, the survey population was divided into non-overlapping parts characterized by the homogeneity of their units. Every part is considered a layer, and every layer is treated as an independent population where a random sample would be drawn separately from every layer. At the end, all drawn sampling units will be integrated to form an aggregate sample.

8.2. Choosing the sample units is done on the basis of the 2010 Establishment Census. In order to choose samples for surveys and statistical studies targeting establishments in general, the framework was divided into four categories on the basis of the establishment’s size as follows:

- Micro-establishments: It includes all establishments that have a workforce of 1-5.

- Small establishments: It includes all establishments that have a workforce of 6-49.

- Medium establishments: It includes all establishments that have a workforce of 50-249.

- Large establishments: It includes all establishments that have a workforce of more than 250.

8.3. The optimal sample unit selection methodology was prepared with the aim of providing high-quality outputs with minimum burden on data providers using methods of rotation and overlap control.

8.4. Required descriptive data are specified to apply the statistical framework and to allocate and choose the sample.

8.5. The sample is tested, assessed and verified, and its use in the current survey round is approved.

|

Sampling Units of Industrial Activity Survey:

The basic sampling units are the enumeration areas. They are sampling units drawn in the first stage of designing the survey sample. Establishments are considered secondary and ultimate sampling units at the same time. They are sampling units drawn in the second stage of designing the survey sample. Each secondary sampling unit is considered a part of the basic sampling units. |

Third stage: Organization:

It is the final preparation stage and precedes data collection. In this stage, the required workflow procedures are established for preparing the finance and insurance survey, starting with the collection stage and ending with the assessment stage and the organization and grouping of those procedures. The optimal sequence of those procedures is chosen to arrive at a methodology that achieves the goals of the statistical product. A review was made in this stage of the procedures that were taken upon the preparation of the previous version of the finance and insurance survey to develop the work procedures in the current version. Those procedures were also described and documented to facilitate any updates in future rounds. The statistical workflow procedures were tested and examined to ensure their compliance with the requirements of preparing the finance and insurance survey, approve the procedures of the statistical workflow, and develop a roadmap for implementation.

Testing the efficiency of input systems and the process of transmitting, synchronizing and reviewing data through either the tablet or office system of the finance and insurance survey are the main procedures in this stage.

Fourth stage: Data collection:

First: The survey sample was chosen through identifying (12,000) establishments as a selected sample that represents the survey population at the level of the Kingdom and is distributed among the thirteen administrative regions of the Kingdom of Saudi Arabia.

Second: The workers, who were nominated as field researchers and visited the establishments to collect data, were chosen on the basis of several practical and objective criteria related to the nature of work, such as:

- Educational level.

- Fieldwork experience.

- Personal attributes, such as: good conduct, evidence of senses and physical and psychological fitness.

- Candidate’s success in the training program of the finance and insurance survey.

- The candidate shall not be under the age of 20.

Third: All candidates (GASTAT staff and collaborators from some government entities) were qualified and trained through special training programs as follows:

- A training program was held for expert staff members in GASTAT headquarters for one week.

- Similar training programs were held for collaborating inspectors, observers, and researchers from all the regions of Saudi Arabia.

| The training programs offered to field researchers tasked with collecting the Industrial Activity survey data include: Practical and hands-on lectures on technical, technological, administrative, and awareness materials that are used in data collection processes. Field researchers are also introduced to the survey’s goals, the data collection method, and how to use maps and reach the holdings. The training programs also include a detailed explanation of all questions on the questionnaire, as well as any technical and administrative tasks. Field researchers are also trained on how to deal with the public and how to ask the questions in record time. |

|

At the beginning of the training program, all trainees are provided with tablet devices that enable them to do the following:

Staff members are nominated to participate in the survey based on their results that are automatically obtained from the “Trainees’ Automated Assessment System” to guarantee promptness, precision, and impartiality upon appointing the candidates and their competences. |

Fourth: The method of direct contact with the establishment was adopted in the process of completing the survey questionnaire and data collection. The field researchers visited the establishments located within the survey sample after arriving at it using the coordinates recorded on the tablets and the guiding maps and introducing themselves and showing official documents proving their statistical identity. They also clarified the aim of their visit, and presented an overview of the survey and its objectives. The electronic questionnaire was then completed orally through direct contact with the owner of the establishment or any official who is familiar with its affairs

Fifth: All field researchers used tablet devices to collect the survey questionnaire data according to timeframes specified based on the number of establishments and their characteristics.

Sixth: Field researchers at all work locations in the Kingdom used the “synchronization” feature available on the tablet devices to download and transfer the completed data of the establishments directly to the database linked to them at GASTAT headquarters where they are stored in a specific way to be reviewed and processed at a later stage.

Seventh: Electronic check rules were applied to guarantee the accuracy, consistency, and rationality of the data entered in the finance and insurance survey questionnaire. They are electronic rules that identify contradictions and they were designed by using a logical link between the answers of the questionnaire and its variables to help field researchers directly identify any errors upon completing the survey data with the official in charge of data provision. Those programmed rules don’t allow any mistakes to go through when an answer contradicts with another piece of information or another answer in the questionnaire.

Eighth: The collected data were verified through being reviewed by the field researcher, their inspector and the survey supervisor in the supervision area. All work areas were subjected to a monitoring and reviewing process from the Data Quality Room at GASTAT headquarters. The room also controls and monitors the performance of all working groups in the field during the data collection process, starting from the first day and until the last.

|

Data Quality Room: An operations room works simultaneously with the field works for the surveys. It is equipped with all sorts of electronic follow-up tools and monitoring and tracking screens. The observers and quality specialists in the room review the consistency of data and detect error cases and extreme values during the data collection process that is taking place in the field. That is done by instantly and immediately following up what is being completed by the field researcher to check the researchers’ commitment to the instructions on the survey, ensure the rationality, accuracy and reliability of data and review some important survey indicators to ensure data accuracy. The room undertakes several tasks, mainly:

Checking the accuracy of the location of completing the questionnaire by matching its coordinates with the ones recorded in the sample file. |

Fifth stage: Disaggreggation:

The disaggregation of the raw data of the Industrial Activities Survey relies on the classification and coding inputs completed during the data collection process, whether they are classified based on the national classification of economic activities, or other classifications such as the distribution of data at the level of administrative regions, or qualitative and descriptive classification based on gender, or social status, or finally quantitative classification based on income groups.

Data related to the Industrial Activities Survey is displayed in suitable tables to facilitate summarizing, understanding and drawing conclusions from them, as well as comparing them to other data, observing statistical significance as they relate to the study’s population, and viewing data without the need to go back the original questionnaires. These tables contain data such as: The names and addresses of establishments and the names of data providers, which violates the principle of statistical data confidentiality.

During this stage, specialists from the department of business statistics conduct data processing and analysis based on several procedures, as follows:

- Sorting and arranging data in a particular sequence or into different groups or categories.

- Summarizing detailed data into key points.

- Combining many data segments and ensuring their interconnection.

- Processing lost or missing data.

- Processing illogical data.

- Converting data into a form that has statistical significance.

- Organizing, presenting and interpreting data.

One of the most important data processing procedures carried out is “data anonymization”. To ensure data confidentiality, GASTAT removes identifiers from the input fields for the survey data, such as hiding the name and address of the establishment owner and other identifiers to protect people’s privacy.

Sixth stage: Revesion:

First: Verifying data outputs:

After reviewing and verifying the accumulated data of the finance and insurance survey, GASTAT conducted at this stage processes of calculating and extracting results and uploaded and stored them on the database. The final reviewing processes were conducted by specialists in financial and investment statistics using modern technologies and software designed for the purposes of reviewing and checking.

Second: Handling of confidential data:

Pursuant to Royal Decree No.23 dated 07/12/1397, GASTAT is committed to the absolute confidentiality of all completed data and not using them except for statistical purposes. Therefore, data are safely stored on GASTAT servers.

|

No individual data on establishments shall be disclosed in any way or form. Materials set for publication are only limited to grouped statistical tables at the level of the Kingdom, the administrative regions and the major cities depending on their features. |

Seventh stage: Publication:

First: Preparing and setting results for publication:

In this stage, GASTAT uploaded the data results from the industrial activities survey database. The Authority then prepared publication tables and graphs for both data and indicators, and added descriptive and methodological information to them. These were prepared in both Arabic and English.

Second: Preparing media material and announcing the bulletin’s release date:

After GASTAT announced the Bulletin’s release date on its official website at the beginning of the calendar year, the Authority prepares the required media materials to announce the Bulletin’s release on all media outlets, as well as its various social media platforms. The announcement will be made on the date set for publication. The bulletin will be published on the official website in various templates of open data in Excel format.

to guarantee its circulation and accessibility to all clients and parties interested in industrial activities. The bulletin is included in the website’s statistics library.

Third: Communicating with clients and providing them with the bulletin:

GASTAT pays great importance to communicating with clients who use its data. Therefore, GASTAT contacts clients upon the release of the finance and insurance survey bulletin to provide them with it. GASTAT also receives questions and enquiries from clients regarding the bulletin and its results through various communication channels. Clients can contact GASTAT to request data. Questions and inquiries are received via:

- GASTAT official website: www.stats.gov.sa

- GASTAT email: info@stats.gov.sa

- Client Support email: cs@stats.gov.sa

- Visiting GASTAT’s headquarters in Riyadh or one of its branches in the regions of the Kingdom.

- Official Letters.

- By Statistical Helpline: (920020081).

Fourth: Preserving the published content:

GASTAT’s Documents and Archives Center stored and archived the data of this bulletin to refer to it at any time on request. GASTAT took that step out of its awareness of the importance of electronically preserving those data to easily refer to them when needed.

Eighth stage: Evaluation:

After the bulletin is released and received by all GASTAT’s clients, the clients are contacted again in this stage which allows for assessing the whole statistical process that was carried out, with the aim of constant improvement to obtain high-quality data. The improvements may include methodologies, processes, systems, statistical researchers’ skill and statistical frameworks. This stage is done in collaboration with data users and GASTAT’s clients through a number of steps:

First: Collecting measurable assessment inputs:

Main comments and remarks are collected and documented from their sources at all stages, including those collected and documented during the collection stage, such as: comments and remarks presented by data collectors and their field supervisors, in addition to data collected and documented during the assessment stage such as the remarks deduced by specialists concerned with reviewing, checking and analyzing data collected from the field. Finally, comments and remarks presented by data users are collected and documented after publication, in addition to what is being monitored via media outlets or the clients’ remarks which GASTAT receives through its main channels.

Second: Making the assessment:

Collected assessment inputs were analyzed, and the results of this analysis were compared with pre-anticipated results. Accordingly, potential improvements and solutions were identified and discussed with experts and concerned parties. In this stage, the performance of clients’ use of the results of the finance and insurance survey and their satisfaction with it is measured. Based on that, recommendations are developed to enhance the quality of the results of the next finance and insurance survey.

Ninth Stage: Management:

A comprehensive stage that spans over all the stages of producing the industrial activities survey. This stage determines the general production plan, including the feasibility study, risk management, means of funding, disbursement mechanisms, as well as developing performance indicators, quality parameters, human resources map necessary for production, following up on the execution of tasks assigned to all departments in every stage, and making reports to ensure that the GASTAT fulfills its commitments towards its clients